ARTICLE • 5 min

IFRS S2 Climate Disclosures: What Companies Need to Disclose About Climate Risks and Opportunities in 2026

July 6, 2026

For many companies, 2026 is a reporting year for climate disclosure. IFRS S2, the climate-related disclosure standard issued by the International Sustainability Standards Board (ISSB), has been adopted or is being actively integrated into national frameworks across Australia, the UK, Canada, Singapore, Japan, South Korea, and beyond. As of April 2026, 28 jurisdictions have adopted the ISSB standards on a voluntary or mandatory basis, with a further 12 planning to do so. If your organisation operates in or reports to a jurisdiction that has moved on ISSB adoption, the question is no longer whether to disclose climate risk, it is whether your disclosures will hold up to scrutiny.

This article breaks down what IFRS S2 actually requires, where companies most commonly fall short, and how to build a disclosure process that is both compliant and credible.

IFRS S2 is the climate-specific standard within the ISSB's sustainability disclosure framework. It sits alongside IFRS S1 (general sustainability-related financial disclosures) and is designed to provide investors and capital markets with consistent, comparable, decision-useful information about how climate risk and opportunity affect an organisation's business model, strategy, and financial outlook.

IFRS S2 draws heavily from the Task Force on Climate-related Financial Disclosures (TCFD) framework, which many organisations are already familiar with. However, it goes further in several important areas, particularly around scenario analysis, Scope 3 emissions, and the granularity of industry-specific metrics.

The standard was issued in June 2023. Jurisdictions began adopting it from 2024, with mandatory reporting timelines varying by country and entity type. In December 2025, the IFRS issued amendments to IFRS S2, and in March 2026 published additional guidance to help companies apply the standard, particularly around climate resilience assessment and scenario analysis.

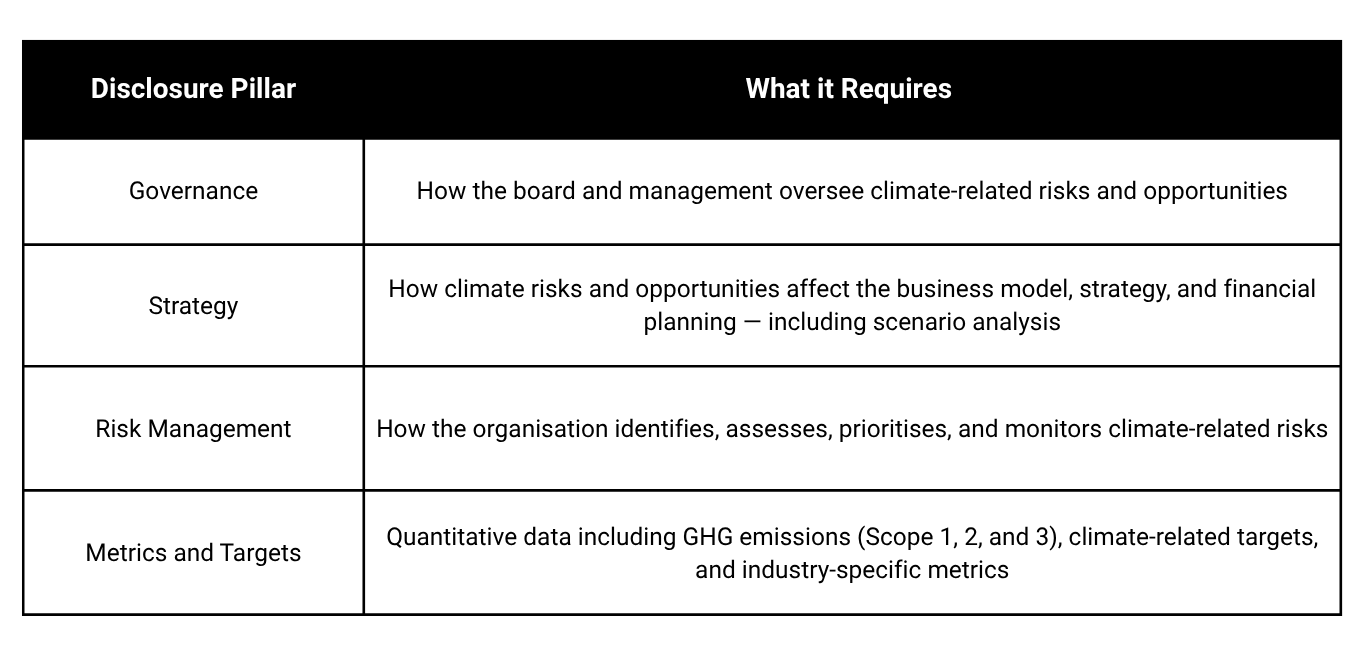

IFRS S2 is structured around four core disclosure areas, directly mirroring the TCFD framework:

Each pillar requires substantive disclosure, not just a statement of intent. Boards cannot simply assert that climate risk is "monitored," they must describe the processes, frequency, and accountabilities that make that oversight real.

IFRS S2 requires organisations to use climate scenario analysis to assess the resilience of their strategy under different climate pathways, including both a below-2°C or 1.5°C scenario and a higher-warming scenario. Many companies complete this analysis once, with external consultants, and do not embed it into ongoing decision-making.

The March 2026 guidance from the ISSB reinforces this point directly: companies must assess their climate resilience on an annual basis, though they are not required to update their full scenario analysis every year. Regulators and auditors are increasingly distinguishing between a scenario analysis that exists as a document and one that is actually integrated into capital allocation, risk appetite, and strategic planning. The former will not satisfy disclosure requirements for long.

IFRS S2 requires disclosure of Scope 3 greenhouse gas emissions for all companies, subject to a materiality determination. For most organisations with complex supply chains, this is the most technically challenging requirement. Value chain data is often incomplete, estimated, or inconsistent across suppliers.

It is worth noting that some jurisdictions are going further than the base standard on Scope 3. Japan's Sustainability Standards Board (SSBJ), for instance, has added a requirement for companies to disclose disaggregated Scope 3 emissions across all 15 categories of the GHG Protocol Corporate Value Chain Standard, which is a more granular requirement than IFRS S2 itself. Companies should begin Scope 3 data collection well before their first reporting date and be transparent in disclosures about the estimation methods and data limitations involved.

A thorough IFRS S2 disclosure requires assessment of both physical climate risks (acute events like floods and cyclones; chronic shifts like rising temperatures and sea level rise) and transition risks (policy changes, technology disruption, shifting market preferences, and reputational exposure). Many organisations default to physical risk because it is easier to map to asset locations, and underinvest in transition risk analysis.

In reality, for many sectors like energy, finance, consumer goods, and manufacturing, transition risks carry greater financial materiality than physical risks in the near to medium term.

IFRS S2 expects organisations to connect climate risks to financial impacts wherever possible. It is not enough to state that flooding is a risk to a coastal facility. Preparers should be working toward quantifying the potential financial exposure: asset impairment, increased insurance premiums, revenue disruption, or capital expenditure required for adaptation.

This is an area where the standard explicitly acknowledges that methodologies are still maturing, but the direction of travel is clear.

One area that distinguishes IFRS S2 from earlier voluntary frameworks is the requirement for industry-specific metrics, drawing on the SASB (Sustainability Accounting Standards Board) standards. This means the disclosure bar is not uniform across industries.

A real estate company, for example, is expected to disclose metrics related to climate-exposed building assets, energy intensity, and portfolio resilience to physical risk. A financial institution must disclose financed emissions and climate-related concentration risk within its lending and investment portfolio. An agricultural company faces specific metrics around land use, water dependency, and supply chain exposure to climate variability.

In March 2026, the ISSB also proposed amendments to SASB standards for three industries — electric utilities and power generators; agricultural products; and meat, poultry and dairy — following earlier amendments proposed in 2025 for extractives, minerals, and processed foods. Organisations in these sectors should monitor these updates closely as they may affect applicable metrics.

Organisations should identify the SASB standard applicable to their primary industry and incorporate those metrics into their IFRS S2 disclosure planning.

For sustainability leaders navigating multiple reporting frameworks simultaneously, understanding how they interrelate is critical.

IFRS S2 and TCFD: IFRS S2 was explicitly built to supersede TCFD as the global standard. In jurisdictions that have adopted IFRS S2, a TCFD-aligned disclosure largely satisfies the equivalent requirements, but IFRS S2 is more detailed in several areas, particularly around scenario analysis methodology and industry metrics.

IFRS S2 and AASB S2 (Australia): Australia's mandatory climate reporting standard (AASB S2) is substantially equivalent to IFRS S2, with some Australian-specific modifications. Australian listed entities and large unlisted companies are already subject to phased mandatory reporting.

IFRS S2 and ESRS E1 (Europe): The EU's Corporate Sustainability Reporting Directive (CSRD) and its associated ESRS E1 standard share significant conceptual overlap with IFRS S2, but differ in scope, double materiality requirements, and disclosure depth. In December 2025, EFRAG submitted draft amendments to the ESRS with an explicit aim of bringing the EU standards closer to IFRS S1 and S2. However, EFRAG has noted that some ESRS reliefs go beyond those of the ISSB standards, meaning organisations seeking to comply with both frameworks should conduct a careful mapping exercise rather than assuming full coverage. A key structural difference remains: the ESRS requires double materiality (considering both a company's financial risks and opportunities and its external impact on the environment and society), whereas IFRS S2 focuses solely on financially material climate information.

IFRS S2 and California SB261: California's Climate-Related Financial Risk Act requires companies with revenues over $500 million doing business in California to disclose climate-related financial risk in line with TCFD. IFRS S2 disclosure largely satisfies the intent of SB261, though specific local requirements should be reviewed.

FRS S2 and Japan (SSBJ): Japan's Sustainability Standards Board (SSBJ) has developed standards explicitly aligned to IFRS S1 and S2, structured as an Application Standard, a General Standard, and a Climate Standard mirroring the ISSB's own architecture. The standards became available for use in 2025, with the Financial Services Agency expected to confirm a phased mandatory timeline for listed companies starting with the largest issuers. Organisations reporting under IFRS S2 should find SSBJ disclosures require only modest adjustment, since the structural alignment is close, though Japan-specific guidance on scenario analysis and transition planning should still be reviewed.

IFRS S2 and Hong Kong (HKFRS S1/S2): Hong Kong has adopted HKFRS S1 and S2, closely modelled on the ISSB standards, with the Hong Kong Stock Exchange mandating climate-related disclosures for Main Board issuers from FY2025 onward, supported by a comply-or-explain transition period for select requirements while companies build capability. GEM Board issuers follow on a later timeline. For companies with dual listings or significant operations across Greater China, Hong Kong's close alignment with IFRS S2 means existing ISSB-based disclosures should transfer with limited modification.

IFRS S2 and Malaysia (Bursa Malaysia): Bursa Malaysia has mandated ISSB-aligned climate disclosures for Main Market listed companies from FY2025, with the ACE Market following on a later timeline. Malaysia's approach reflects the broader ASEAN movement toward ISSB convergence, coordinated through the ASEAN Capital Markets Forum, meaning IFRS S2 disclosures should map closely onto Bursa's requirements with limited jurisdiction-specific adjustment needed.

IFRS S2 and the UK (UK SRS): The UK government published its final UK Sustainability Reporting Standards (UK SRS S1 and S2) in February 2026, closely modelled on IFRS S1 and S2 with a small number of UK-specific amendments. The standards are currently available for voluntary use, and the Financial Conduct Authority has proposed making UK SRS S2 climate disclosures mandatory for listed companies from accounting periods beginning on or after 1 January 2027, with final rules expected in autumn 2026. Broader UK SRS S1 disclosures and Scope 3 emissions are proposed to follow on a comply-or-explain basis with transition relief. For companies already reporting under IFRS S2, UK SRS should require limited rework given the close structural alignment, though the mandatory timeline is not yet finalised and should be tracked through the FCA's autumn 2026 policy statement.

IFRS S2 and Singapore (status: partially delayed): Singapore has not adopted IFRS S1 or S2 directly into law, but has embedded IFRS S2's climate-related requirements into SGX Listing Rules. Scope 1 and 2 emissions reporting remains mandatory for all listed companies from FY2025, and Scope 3 reporting remains mandatory for Straits Times Index (STI) constituents from FY2026. However, in August 2025 regulators delayed the broader rollout for the remaining listed market by up to five years, citing global economic uncertainty and limited readiness among smaller companies, with Scope 3 disclosure remaining voluntary for non-STI companies until further notice and other ISSB-aligned disclosures pushed to FY2028 or FY2030 depending on market capitalisation. This means Singapore is "live" only for the largest listed companies; the broader market timeline has genuinely slipped.

IFRS S2 and Canada (status: paused, not merely delayed): Canada's Sustainability Standards Board finalised CSDS 1 and CSDS 2 in December 2024, closely aligned with IFRS S1 and S2 with additional Canadian transition reliefs. However, these standards remain entirely voluntary. In April 2025, the Canadian Securities Administrators paused work on a mandatory climate disclosure rule, citing uncertainty in the global regulatory environment including developments in the US and EU, and no rulemaking timeline has been set. There is no confirmed mandatory date at all, only an expectation that the CSA will eventually revisit the question. Only voluntary CSDS reporting is available and increasingly expected by investors in the interim.

Meeting IFRS S2 disclosure requirements is not a once-a-year reporting exercise. It requires embedding climate risk assessment into ongoing organisational processes. The organisations that will produce credible, auditable disclosures are those that:

The manual approach to climate risk assessment — spreadsheets, consultants, point-in-time analysis — is increasingly inadequate for meeting the ongoing, auditable disclosure requirements of IFRS S2. Companies that rely on bespoke consulting engagements for each annual disclosure cycle face not only significant cost, but also the risk of inconsistency and methodology gaps that will be difficult to defend under external assurance.

Purpose-built climate disclosure platforms enable organisations to automate the physical and transition risk and opportunity assessment process, overlay risk data on specific asset locations, model financial impacts under multiple scenarios, and generate disclosure-ready outputs within a single, auditable workflow. This is particularly important as disclosure obligations shift from voluntary to mandatory, and as auditors and regulators raise the bar on what constitutes a credible climate disclosure.

Looking ahead, sustainability leaders should be aware that the ISSB's scope is expanding beyond climate. Following its announcement in late 2025, the ISSB is planning to publish draft requirements and guidance for nature-related reporting in Q4 2026, timed to coincide with the UN's COP17 biodiversity conference in October. The guidance will draw on the work of the Taskforce on Nature-related Financial Disclosures (TNFD) and is intended to complement IFRS S1 and S2, explaining how companies can disclose nature-related information within the existing standards. It is expected to take the form of an IFRS Practice Statement rather than a new mandatory standard, though individual jurisdictions could still choose to mandate it.

For organisations already building climate disclosure infrastructure, this is a signal to design systems and processes with broader sustainability disclosure in mind from the outset.

IFRS S2 represents the normalisation of climate risk and opportunity as a financial disclosure obligation. For sustainability leaders, the priority in 2026 is building the systems, data, and processes to produce disclosures that are credible, consistent, and audit-ready.

The companies that invest in that infrastructure now will not only meet their compliance obligations; they will be better positioned to demonstrate climate resilience to investors, lenders, customers, and regulators who are increasingly treating climate disclosure as a proxy for management quality.

Socialsuite's Climate Risk Assessment and Scenario Analysis module is purpose-built for IFRS S2, ASRS S2, TCFD, CSRD, and SB261 disclosure requirements. It automates physical and transition risk assessment, scenario analysis, and disclosure reporting in a single integrated platform.

Whether it’s a public company, a private company, or a charity, Socialsuite has the right solution for you.